Fixed Income

In the third quarter of 2017, fixed income markets continued to be well supported by a number of factors including accommodative central bank policies, positive growth, and few signs of an acceleration in inflation. Additionally, markets were also boosted by low volatility across equity and fixed income, and confidence even with regards to potential political risks. However, during the end of the quarter investor sentiment and appetite declined moderately mainly due to geopolitical developments. In Europe, benchmark yields have trended higher and the yield curve continued to steepen slightly. The pace of withdrawal of Quantitative Easing (“QE”) is still expected to remain very gradual as inflation remains below target, ticking higher as growth dynamics improved. Tapering indications are expected to be given in October. Comments from the European Central Bank’s (“ECB”) president, Mario Draghi on the strengthening of the Euro currency and how it is affecting inflation and growth in the euro zone were interpreted as not particularly “dovish”.

In the US, the Federal Reserve (“Fed”) raised interest rates by 25bps to 1.00%-1.25% in mid-June and the intention for the Fed to raise rates by the end of the year remains, with expectations of an increase of another 25bps.

US bond markets continued to be dominated by the diverging messages from the Fed and the US Treasury (“UST”) bond markets. The Fed has generally maintained its signals towards higher rates and announced that it will begin shrinking its US$4.5 trillion balance sheet in October. This will be done by not reinvesting maturing bonds which will initially amount to US€10 billion. On the other hand, bond markets seem to be focusing on geopolitical concerns and low inflation expectations, despite higher than expected data in August.

In line with recent months, the underlying view is that markets should expect to receive less of a boost from central bank actions compared to recent years. The ECB is expected to remain more active in maintaining a “cap” on rising yields than the Fed. Investors should moderate expectations in terms of capital upside, whilst further spread compression seems possible even though credit spreads are already near all-time lows. Rising benchmark yields are likely to have a negative impact on total returns particularly in the sovereign and Investment Grade (“IG”) sectors. The High Yield (“HY”) market, despite being well supported, has experienced a slight slowdown in returns during Q3 and as noted in the previous update, HY could be more vulnerable to some correction in comparison to early 2017.

The euro yield environment has so far undergone less of a re-pricing of a future potential turnaround in monetary policy. This, together with the differential in carry, makes Euro IG slightly less attractive compared to USD IG. The HY market is in a more advanced stage of the credit cycle, and even though fundamentals remain positive the additional attractiveness of HY compared to IG and sovereign markets has diminished.

Equities

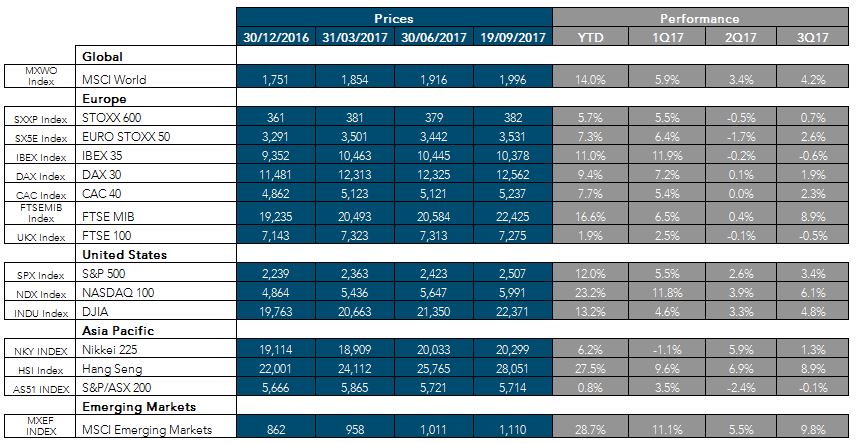

All equity indices under review have returned a positive performance year to date. The theme this year has been to buy growth in a World absent of any meaningful economic growth, which can be evidenced by the performance in the indices below. The Emerging Market index has been the top performer year to date with a return of 28.7%, followed by the Hang Seng with 27.5% and the Nasdaq with 23.2%. After a lukewarm second quarter with an average return of -0.3%, investors have looked at Europe for alpha. The top performer this year has been Italy with a 16.6% improvement.

Source: Bloomberg

Economic and political scenario: The economic and political situation has been supportive of the stock market so far this year. Economic data in Europe has generally been better than expected while elections, which at the start of the year were an overhang for the European equity story, have provided no negative surprises.The US economy continues to grow, supported by high consumer spending and business investment which has helped to push down unemployment to levels not seen for many years. On the fiscal policy front, debt limit talks in December could create some uncertainty. Recently, two Senators said that they have agreed to a tentative deal that would allow headroom for a significant tax cut (rumour - $1.5trillion). There has been no update on the infrastructure project.

Valuations: US valuations are looking stretched. The S&P 500 index is trading on a forward P/E ratio of 17.3x, the highest reading in the past 10 years. The equity valuations in Europe are less expensive but not cheap as the STOXX 600 index is trading on a forward PE ratio of 14.7x which ranks in the 94th percentile in the past 10 years.

It is also worth mentioning that bear markets don’t always follow a recession (Cyclical). Bear markets may also be triggered by certain events (one-off shock like war, oil price shock etc) or due to structural problems (structural imbalances and financial bubbles). According to Goldman Sachs, since the 1800’s there have been 16 cyclical bear markets, 7 structural and 7 event-driven. The last cyclical bear market was in 1990. Since then we had 2 event driven (1998 – EM Crisis and 2011 – Euro Debt Crisis) and 2 Structural (2000 – dot.com bubble and 2007 – Housing bubble). The point to take here is that an improving macro-economic backdrop does not necessarily imply a lower risk of a bear market.Despite this, a more realistic scenario would be for equity markets to perform well but with an uptick in volatility. The high valuations together with low inflation (when compared to other bull markets in the past) and interest rates suggest lower potential positive returns in the near term. Should inflation expectations change, and higher interest rates needed, the probability of a bear market would increase.

Key risks to the above views:

- Lack of development regarding the US infrastructure projects and tax cuts that have been priced in by the market;

- Increase in international geopolitical risk especially North Korea;

- FED falling behind the inflation curve which could lead to aggressive tightening;

- China hard landing;

- Weakness/volatility in energy, commodities, EM currencies;

- Setback within Eurozone (Brexit negotiations, Italian banks);

- Euro continues to strengthen (EURUSD 1.30 could be a problem).

The information presented in this commentary is solely provided for informational purposes and is not to be interpreted as investment advice, or to be used or considered as an offer or a solicitation to sell/buy or subscribe for any financial instruments, nor to constitute any advice or recommendation with respect to such financial instruments. Curmi and Partners Ltd. is a member of the Malta Stock Exchange, and is licensed by the MFSA to conduct investment services business.