By Robert Ducker

The current economic cycle is the second longest on record at 113 days and is set to become the longest in the third quarter of 2019. The new trend of longer and gradual growth seems to have replaced the quick and strong turnarounds seen in the previous cycles.

The US economy has probably passed its peak growth levels as the unemployment rate is very low compared to history with little scope for further declines. Real wages have been growing consistently since February 2017, averaging around 1.0% year-on-year in 2018 compared to a real wage growth of 0.7% in 2017. Similarly, inflation averaged 2.1% in 2018 up from 1.9% in 2017. Labour participation rate is still well below pre-crisis levels, but has been stable at around 62.9% over the past four years. The low unemployment rate has been a major driver for consumer spending, and we expect this to continue in 2019. Consumer spending is an important contributor to GDP growth. ISM PMI has been volatile this year but is still well above 50.0x. Any reading below 50.0x would represent contraction over the previous month.

The Business cycle

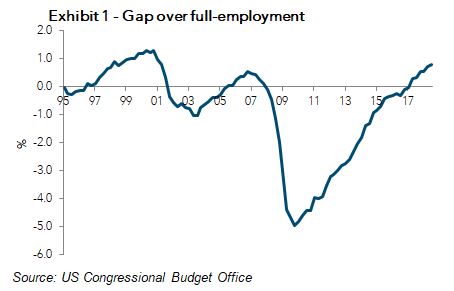

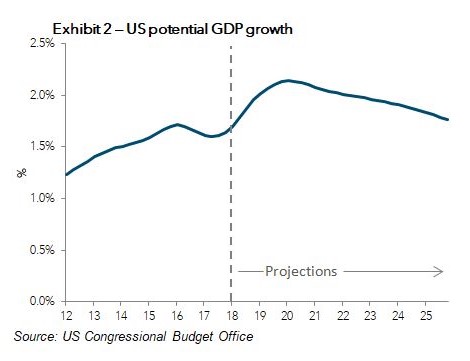

The US economy has advanced through the cycle at a faster rate than the other major economies. The real economic growth rate recorded in the third quarter of 2018 of 3.0% and the estimates for the upcoming years are above potential GDP of 2.0% (Source: US Congressional Budget Office) apart from 2020. Additionally, the current unemployment rate is 0.8 percentage points below the FED’s long-run estimate of 4.6%. This is a sizeable gap by historical standards, with the average gap since 1960 at -0.5 percentage points, i.e. actual unemployment has historically been above the long-run estimate on average. You would have to go back to the period between 1998 and 2001 to find a similar gap. The tight labour market indicates higher wages and higher price levels. The Core PCE price inflation has softened since the summer, currently at 1.8%, which is still close to the 2% target, with the tariffs possibly leading to higher goods pricing in the near term.

All of the above suggests that the US economy needs to slow down slightly to avoid overheating. The impact from fiscal policy is likely to diminish in 2019, but the low unemployment rates and high consumer confidence should continue to be tailwinds. This is where the FED comes in.

FED has continued to tighten despite clouded outlook

As mentioned earlier, 2018 will be remembered for all things negative in relation to political developments. The market in general has been wary of the potential impact from a trade war and the economic slowdown in Europe and China. The FED was unmoved however, hiking rates 4 times in 2018.

Many investors including President Trump have urged the FED to re-consider the interest rate path in view of the softer global macro-economic prospects. However, bearing in mind where the US is the economic cycle, we believe that the FED is unlikely to alter its tightening stance significantly. Currently the FED dots are indicating two rate hikes in 2019.

Impact on Emerging Markets

The spill over on emerging markets from a hawkish FED could be significant, as the stronger Dollar could have a negative impact on their respective currency. Most EM countries borrow primarily in US Dollar, with any strengthening of the dollar increasing their debt to GDP in local currency. This could be a concern for EM growth, but could be considered as less risky than the US economy overheating which would lead to a faster hiking path.

The information presented in this commentary is solely provided for informational purposes and is not to be interpreted as investment advice, or to be used or considered as an offer or a solicitation to sell/buy or subscribe for any financial instruments, nor to constitute any advice or recommendation with respect to such financial instruments. Curmi and Partners Ltd. is a member of the Malta Stock Exchange, and is licensed by the MFSA to conduct investment services business.