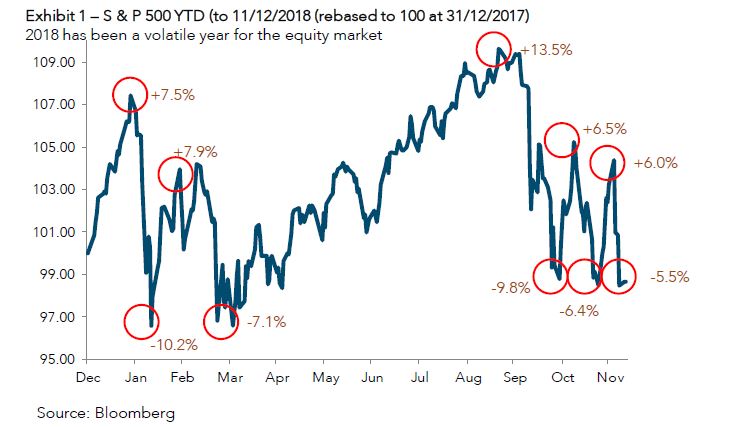

The equity market performance was negatively affected by accelerating political risk, uncertainty over FED policy and concerns over global macro-economic outlook during 2018. Contrary to 2017, which saw subdued volatility, 2018 was characterised by large daily swings, with the S&P 500 surging 7.5% in the first three weeks of the year but then reversing sharply with a 10.2% decline over the next week reaching a low for the whole of 2018 on the 8th of February.

Macro-economic growth respectable in 2018 despite equity market performance

Investor confidence has been dented by rising political risk and weaker economic data published by big economies particularly the EU and China. However, looking through the noise, 2018 has been a good year for the global economy. Consensus is currently looking for global real economic growth of 3.7% in 2018, which would equal the growth registered in 2017 and well above global potential growth rate of 2.5% according to the World Bank (potential growth for period 2018 to 2027). The main driver of economic growth remains emerging markets, with 5.0% expected in 2018 (2017: 4.9%). Growth in developed economies is expected at 2.3%, slightly below 2017. The main laggards are expected to be Japan, the Euro zone and the United Kingdom.

Europe’s economy has been weaker this year but much of this weakness can be explained by one-offs (weather, sickness and industrial action in the first half of the year and new vehicle emissions standards on the 1st of September). Yellow vests protests could lead to further weakness in the fourth quarter of the year. Europe’s 2019 economic outlook will largely depend on trade talks, especially when considering Germany’s dependency on trade. Falling unemployment has been a clear positive for the Europe which could boost consumer spending in the near term.

A nightmare for Central bankers

Central bankers are in the process of normalising monetary policy, which is not a simply feat as a misstep could have severe consequences on economic growth prospects. The current chaotic backdrop is no doubt undesirable. The FED has now moved well above zero, raising interest rates 8 times since 2015. Meanwhile, the ECB will probably delay any tightening over the next 12 months, despite indications early in 2018 that monetary policy normalisation could start this year.

Equity valuations look more attractive

Most equity indices were down on a year to date basis in 2018. The Dax index, an export oriented index, was the worst performer, losing 18.3% on a total return basis, highlighting the main investor concern throughout the year. Share prices fell at a faster rate than earnings during 2018 which could indicate a sentiment driven sell-off.

Based on data extracted from Bloomberg, equities have cheapened significantly since the start of the year. This implies that share price declines have been faster more severe than negative earnings revisions. The flipside could be that expected earnings are overstated (or that Bloomberg expected earnings are outdated) and a lot will depend on whether there is a successful conclusion to the trade talks between the US and China.

We believe that equity markets should perform well over the next 12 months but see elevated risks. In our opinion the weakness in the equity market during 2018 was more sentiment driven rather than a significant change in fundamentals. The base case is still for earnings to grow in 2019, assuming no deterioration in US/China relationship and excluding an uptick in tensions between US/EU (auto tariffs).

The information presented in this commentary is solely provided for informational purposes and is not to be interpreted as investment advice, or to be used or considered as an offer or a solicitation to sell/buy or subscribe for any financial instruments, nor to constitute any advice or recommendation with respect to such financial instruments. Curmi and Partners Ltd. is a member of the Malta Stock Exchange, and is licensed by the MFSA to conduct investment services business.