Article by David Curmi

It is now some 27 years since the Malta Stock Exchange first started its operations back in January 1992. Using the human analogy, the MSE is now well passed its teenage years and though perhaps not fully matured, is well on the way to becoming a mature adult.

Being a mature adult from an age perspective, does not capture the experience that the collective market has and perhaps from an investment cycle perspective we are probably still tuning our skills. In fact, I often hear the comment that the local market is still a very immature one. What makes a mature market though? If I had to have a stab at defining this I would argue that a mature market is one that acts rationally. Naturally a market that acts rationally, and which subscribes to the efficient market hypothesis, may not reconcile itself to behavioural finance theory where the actions are influenced by human emotion and cognitive fallibility. Purely from my experience of being in the market since it began in 1992, it is difficult to argue that the local stock market acts rationally. There are many examples of this, but perhaps one that arises quite frequently relates to the proper pricing of risk. In other words, are investors being adequately compensated in the return they are expected to make from an investment for the risk they are taking?

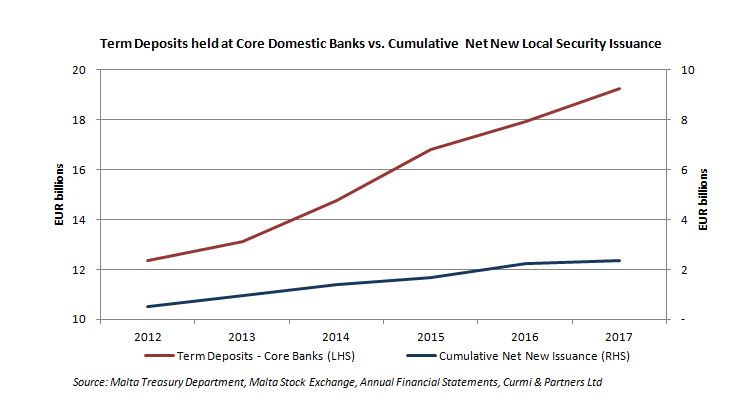

2019 promises to be one of the most active years on record from a new issue perspective. The indicative listing calendar published by the Malta Stock Exchange earlier this weeks indicate no less than 9 new corporate bonds issuing a total of €209m of new paper. This is great news for the market in that it boosts investor choice, creating both width and depth to the market. It appears that the concept of a listing on the Malta Stock Exchange has now reached wider appeal and one hopes that the rate of issuance will continue. The reality of a government that is not issuing new government stocks due to the balanced budget that it is operating at has left a gaping hole for investors to be filled, especially at a time when interest rates do not look like they are on the rise any time soon. Recent European economic data unfortunately shows economies that continue to stutter. Meanwhile cash deposits (see chart) continue to climb, at a faster rate than new issues are coming to the market, and from a larger base, indicating the growing capacity of cash to find a home in a locally quoted investment.

The availability of new bonds also provides investors with optionality on their existing holdings. It allows investors to compare the price and value of their existing bonds with the new ones coming to the market. This in itself should help in the process of identifying, with the help of advisers, which investment opportunity provides a better risk return ratio. It always comes as somewhat of a surprise to me that despite glaring disparities in the quality of bonds on the market that investors do not appear to make more of a distinction between the good and the bad. Or perhaps it is my analysis of what is good and bad that is flawed!

A more active approach to the analysis and pricing of risk is desperately needed. In the long term this will help better align expectations and outcomes, thus helping to avoid surprises. It will also act as a great discipline on companies who, due to having to pay a realistic rate of interest (the price of money) will be more discerning in the application of such funds.

I remain optimistic that investors will ultimately learn to make the right analysis, or find the right entity to do this on their behalf. In the property market this appears to be happening. If one had to peel away the layers of froth in the local property market you will still see that there are clearly pricing differences on what are deemed to be quality properties in quality areas. This basic premise ought to filter itself back to all types of investments. Quality investments should command a higher price. I live in eternal hope.

The information presented in this commentary is solely provided for informational purposes and is not to be interpreted as investment advice, or to be used or considered as an offer or a solicitation to sell/buy or subscribe for any financial instruments, nor to constitute any advice or recommendation with respect to such financial instruments. Curmi and Partners Ltd. is a member of the Malta Stock Exchange, and is licensed by the MFSA to conduct investment services business.