By Matthias Busuttil

At its monetary policy meeting on 7th March, the Governing Council of the European Central Bank (ECB) announced measures intended to sustain easy financing conditions and to maintain interest rates at rock-bottom levels, beyond what was previously anticipated. This communication by the central bank comes at a time when risks are pointing towards a challenging year for the European economy.

Along with the termination of the ECB’s quantitative easing programme towards the end of 2018, which contributed to a monetary injection of EUR 2.6 trillion over the last four years, the ECB had guided towards the possibility of a first rate hike in the euro area occurring after summer of 2019. These were the first signs that the ECB is slowly shifting towards a normalising monetary regime as the European economic recovery was underway.

However, as the outlook for the European economy started to worsen and the weakening price pressures are likely to dampen inflation once again, the ECB reacted by communicating a renewed commitment of monetary support. The ECB has extended its forward guidance to maintain its key interest rates unchanged “at their present levels at least through the end of 2019”. This pushes the projection for the first rate increase in the euro-area out to the first quarter of 2020 at the earliest.

Moreover, the ECB announced the launch of a bank lending operation, named “Targeted Longer-Term Refinancing Operation (or TLTRO-III). This is the third time that the ECB will undertake such a programme and it is intended to provide cheap financing to European banks that is linked to their level of lending activity. This programme is aimed at providing financing to banks to sustain their loan provisioning functions during times of economic weakness which may put pressure on other sources of finance.

The change in the forward guidance on interest rates as well as the launch of TLTRO-III effectively marks a u-turn in the central bank’s original plan to move towards a less accommodative monetary regime.

Investor reaction tends to be positive with such news given that an easy monetary environment supports higher asset valuations. However, in this case, investors were spooked with the ECB’s assessment of the economic and inflation outlook.

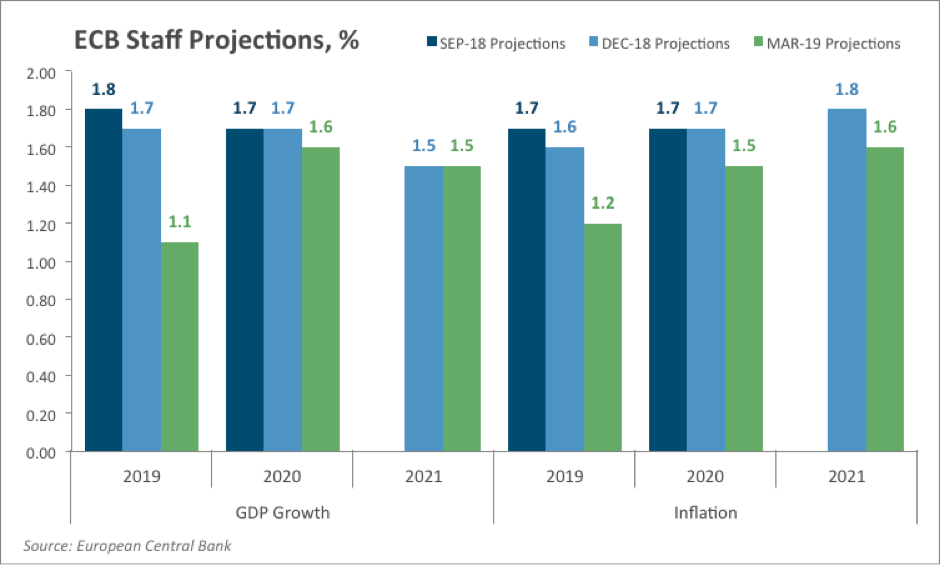

Market participants did expect a downward revision in the ECB’s quarterly economic growth and inflation projections update. However, the extent of the downward revision in the projections published in March paints a gloomier picture than anticipated by investors. As shown in the embedded chart, the new projections are forecasting an economic growth rate of 1.1% in 2019, 1.6% in 2020 and 1.5% in 2021, compared to the higher December projections of 1.7%, 1.7% and 1.5% for 2019, 2020 and 2021 respectively.

Similarly, inflation rate projections are now at 1.2% for 2019, 1.5% for 2020 and 1.6% for 2021, while the December projections predicted healthier inflation rates of 1.6%, 1.7% and 1.8% in 2019, 2020 and 2021 respectively.

The change in projections, which consequentially underpinned the ECB’s decision to switch tack, was primarily the result of external factors and internal factors, to a lesser extent, that are negatively impacting the pace of the economic expansion. Specifically, the ECB cited the persistent uncertainties related to geopolitical factors and the threat of protectionism, mainly referring to US-China trade tensions and Brexit, as well as weakness in emerging economies. These external factors, together with Italy slipping into recession and Germany only narrowly avoiding one in Q4 2018, have deteriorated economic sentiment in Europe which is considerably reliant on external demand and exports.

Although the weak economic projections bring back recollections of the not-so-distant history of the European economy, the main worry this time is the lack of ammunition or tools available for the ECB to combat another economic downturn.

The ECB is not the only central bank to have changed route over the last few months. As the risks of a global economic slowdown increased, the US Federal Reserve has also decided to halt interest rate increases for the time being and to be more patient in ascertaining the health of the economy prior to resuming its rate hike cycle.

The information presented in this commentary is solely provided for informational purposes and is not to be interpreted as investment advice, or to be used or considered as an offer or a solicitation to sell/buy or subscribe for any financial instruments, nor to constitute any advice or recommendation with respect to such financial instruments. Curmi and Partners Ltd. is a member of the Malta Stock Exchange, and is licensed by the MFSA to conduct investment services business.