By Matthias Busuttil

Almost a decade into the recovery from the great financial crisis, and following years of ultra loose monetary policy, inflation seems to be numb to the economic developments achieved so far particularly in the US.

With the economy growing at above average growth rates quarter after quarter and unemployment running at very low levels for an extended period of time, monetary authorities are still grappling with low inflation as price pressures struggle to gain steam.

The Federal Reserve’s preferred measure of inflation, as calculated via the personal consumption expenditure (PCE) index, was at 1.6% in March ’19, coming down from 2% in June ’18 – the highest it has been since the peak in March ’12. In fact, during the economic expansion since 2009, the average core PCE inflation rate was of circa 1.5%, materially undershooting the Fed’s target of 2%.

The Federal Reserve has long maintained that upward price pressures would result from the tight labour market conditions while the economic slack is reeled back in. In anticipation of this, the Fed has increased interest rates nine times over the last three years and initiated a gradual wind-down of its balance sheet.

The persistently low inflation readings have been explained as being temporary and mainly the result of transitory factors. However, as self-doubt is starting to creep in, the Fed has put interest rate increases on hold at its March policy meeting while Jerome Powell, Fed Chairman, emphasised on maintaining a patient stance for the time being.

The minutes of the March meeting published on Wednesday 22nd, show that policy makers are willing to maintain interest rates unchanged, even if there is an improvement in economic conditions.

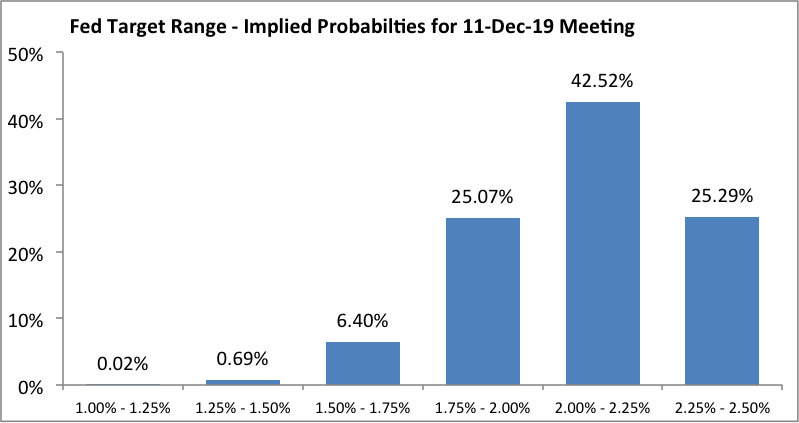

Market participants have a slightly different idea on the Fed’s course of action for the rest of the year. The future-implied probabilities, as illustrated in the embedded bar chart, show that the market expects a higher chance of a rate cut by the end of the year from the current policy range of 2.25% - 2.50% to 2.0% - 2.25%.

Source: Bloomberg

The minutes also show that a number of members are becoming anxious about subdued inflation expectations remaining stuck below the Fed’s target. The minutes noted that “several participants commented that if inflation did not show signs of moving up over coming quarters, there was a risk that inflation expectations could become anchored at levels below those consistent with the Committee’s symmetric 2 percent objective”.

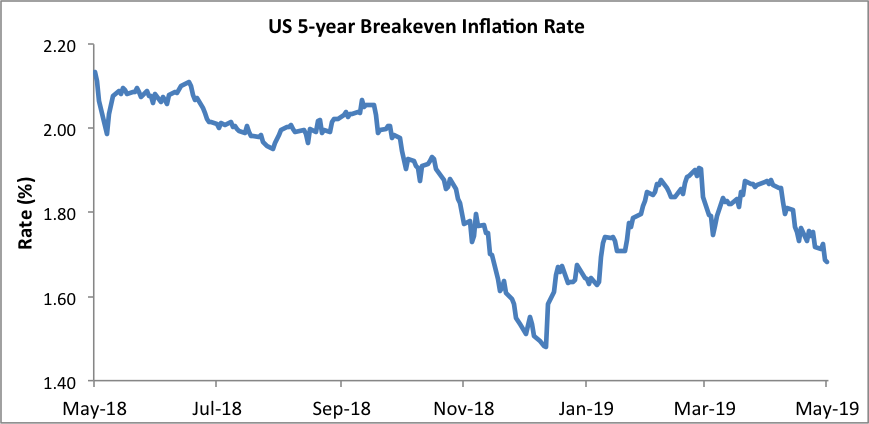

The conventional measure of assessing inflation expectations, the five year breakeven rate on US Treasuries, showed a pronounced rebound since the start of the year reflecting positive expectations of an economic recovery and higher expectations of a successful conclusion in trade discussions.

Source: Bloomberg

However the trend reversed in mid-April. The correction in inflation expectations coincided with the escalation of the trade tensions with China casting further doubt on the rate of global economic expansion and corporate earnings during the second half of the year.

While transitory factors may have suppressed inflationary pressures in the short term, it is becoming increasing evident that other less cyclical forces are at play. Policy makers have cited insufficient aggregate demand far too long as the reason for subdued inflation giving little regard to supply-side forces including the technological events, demographical and political evolutions which are structurally shifting the economic paradigm. The Fed has taken its first step in revising its approach in assessing the economy by launching a review of its policy framework this year.

The information presented in this commentary is solely provided for informational purposes and is not to be interpreted as investment advice, or to be used or considered as an offer or a solicitation to sell/buy or subscribe for any financial instruments, nor to constitute any advice or recommendation with respect to such financial instruments. Curmi and Partners Ltd. is a member of the Malta Stock Exchange, and is licensed by the MFSA to conduct investment services business.